METHODOLOGY

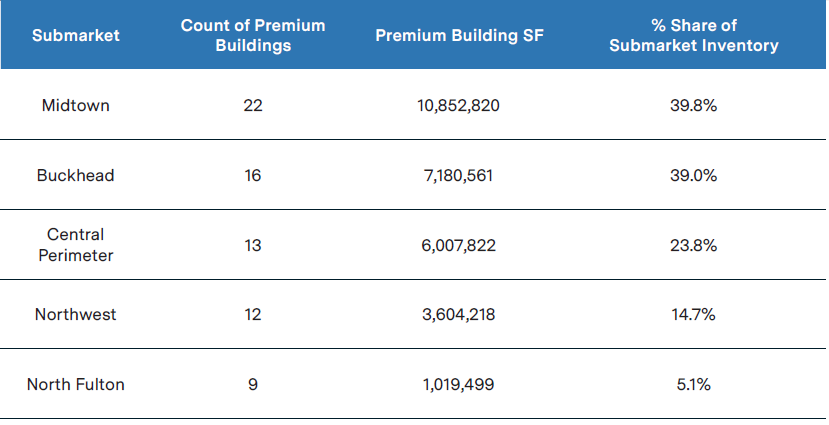

Partners’ research and brokerage teams worked jointly to define premium properties within the following submarkets: Midtown, Buckhead, Central Perimeter, Northwest, and North Fulton.

The resulting analysis examines market dynamics within the selected premium buildings. To qualify as premium, buildings must satisfy the following location and physical quality benchmarks:

Location Quality

- Direct proximity to either transit or highways

- High Walk Score or amenity density

- Near retail | dining

Physical Quality

- Modern construction or has undergone substantial renovation

- Desirable exterior architecture

- Large, efficient floorplates

- Building level amenities like a fitness center, on-site food & beverage options, tenant lounges/meeting rooms/collaboration spaces, rooftop/outdoor terraces, or activated lobby spaces

Premium Product Thrives in Key Submarkets

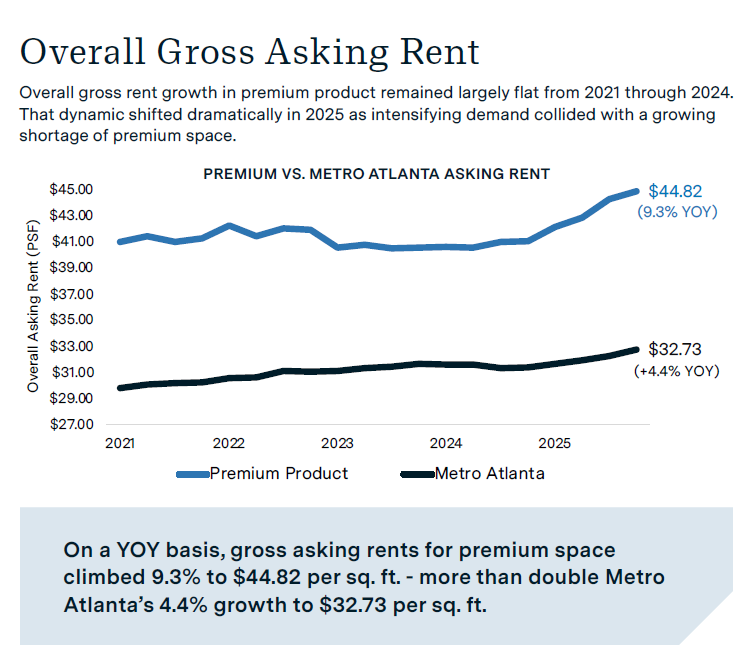

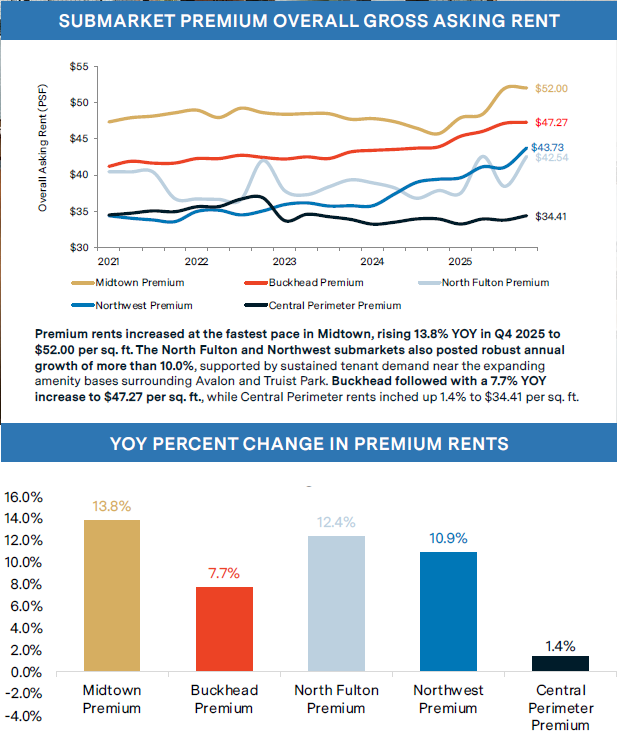

Strong demand has continued within premium office product across Atlanta’s key submarkets, driven by employers’ focus on attracting and retaining top talent through workplace locations that offer rich lifestyle and convenience features. The bifurcation in demand toward the top end of the quality spectrum has spurred an acceleration in occupancy growth, resulting in significant vacancy compression and robust rental rate growth. As demand continues to concentrate in premium product amid a prolonged slowdown in new construction, availability constraints are poised to intensify across Atlanta’s most highly amenitized, well-located assets in the coming years, ultimately restoring conditions needed to support new development.

KEY TAKEAWAYS

- Net absorption in premium product has surged to nearly 2.2 million sq. ft. since 2021, reinforcing sustained leasing momentum in premium product.

- Absorption strength has placed downward pressure on vacancy in premium buildings, which maintain rates well below their respective submarkets.

- Driven by sustained occupier demand, premium asking rents have risen to

new historic highs in most key submarkets.

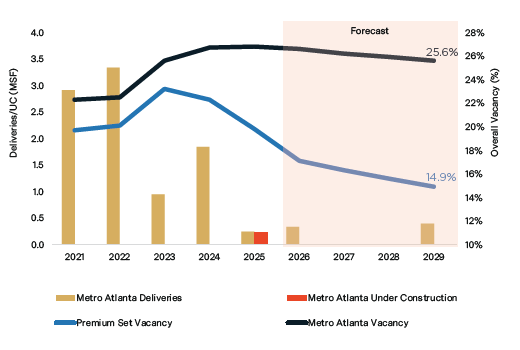

Atlanta Overall Vacancy & Deliveries

As return-to-office mandates continued to proliferate amid historically low construction activity, office vacancy in premium product improved significantly last year. Premium office vacancy declined by 250 bps YOY in Q4 2025 to 19.8%, a four-year low and well under the metro-wide rate of 26.8% (+10 bps YOY). With 250,000 sq. ft. of space completed in Metro Atlanta in 2025 and only 332,000 sq. ft. of speculative office product slated to deliver through 2028, vacancy in premium buildings is expected to decline to under 15.0% in 2029.

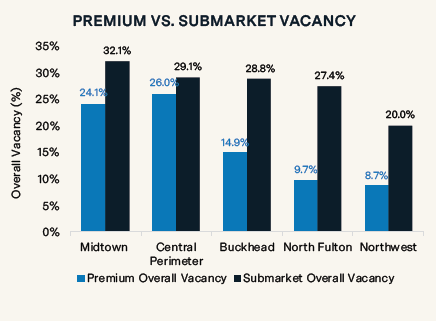

SUBMARKET VACANCY

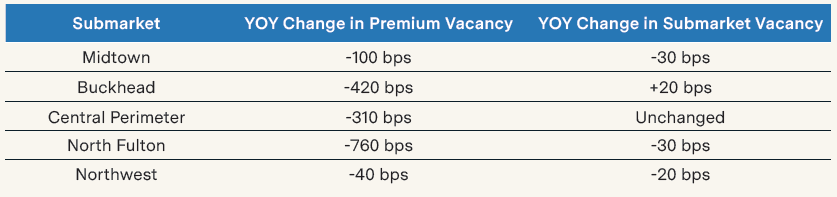

Vacancy compression has been most pronounced in suburban Atlanta, where a surge in occupancy and minimal new construction in recent years has reduced availability. Nowhere is this trend more pronounced than in North Fulton, where vacancy in premium buildings declined by 760 bps YOY in Q4 2025 to 9.7%, well below the 27.4% (-30 bps) rate in the broader submarket. Central Perimeter premier vacancy registered a 310-bps decline to 26.0%, while Northwest vacancy dipped 40 bps to 8.7%, less than half the submarket rate of 20.0%. In Buckhead, premier vacancy plunged 420 bps to 14.9%, also less than half the submarket average of 28.8%. Midtown followed suit, as a 100-bps YOY decline drove premier vacancy down to 24.1%.

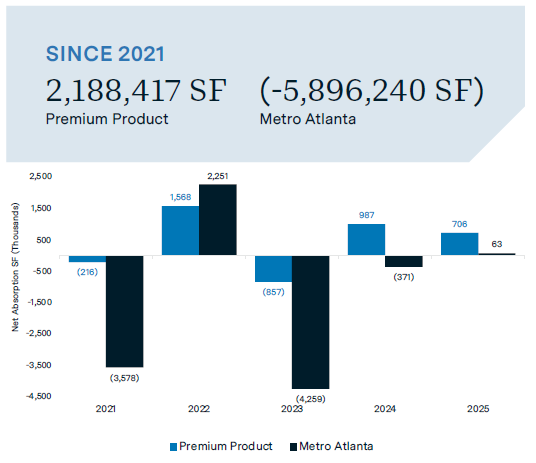

Atlanta Net Absorption

Premium officce occupancy has rebounded sharply in the two years since declining in 2023 as tenants have increasingly prioritized strong amenity packages and flexible layouts. Net absorption in premium buildings totaled 986,853 sq. ft. in 2024 and remained strong at 706,226 sq. ft. in 2025. By comparison, Metro Atlanta recorded 371,221 sq. ft. of occupancy loss in 2024 and 62,676 sq. ft. of gains in 2025. Since 2021, premium occupancy growth has totaled nearly 2.2 million sq. ft., a sharp contrast to Metro Atlanta’s 5.9 million sq. ft. of negative net absorption in that time.

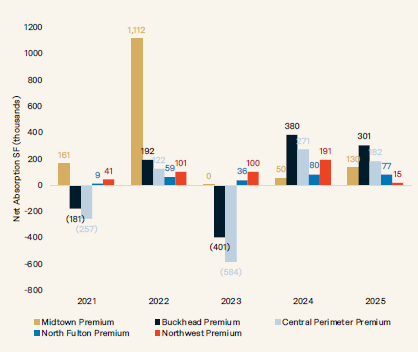

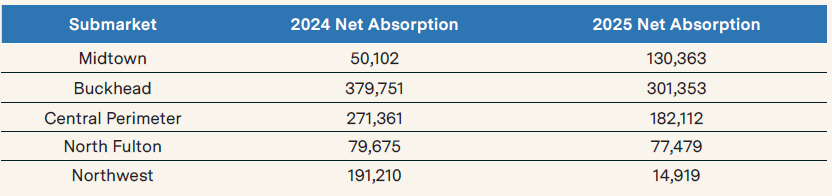

PREMIUM SUBMARKET NET ABSORPTION

Occupancy levels have surged in the CBD, reflecting tenant preference for walkability and access to retail/dining. Buckhead led all submarkets with more than 300,000 sq. ft. of premium net absorption in both 2024 and 2025, while Midtown boasted 50,102 sq. ft. of occupancy gains in 2024 and 130,363 sq. ft. in 2025. Since 2021, Midtown premium buildings have documented nearly 1.5 million sq. ft. of net absorption, most among the five submarkets in this study. In the non-CBD, Central Perimeter tallied 271,361 sq. ft. of occupancy gains in 2024 and 182,112 sq. ft. in 2025, both highs among suburban submarkets. Northwest notched 191,210 sq. ft. of net absorption in 2024, though the pace of occupancy moderated to 14,919 sq. ft. in 2025. In North Fulton, premium net absorption remained consistent at just under 80,000 sq. ft. in both 2024 and 2025.

Total Leasing

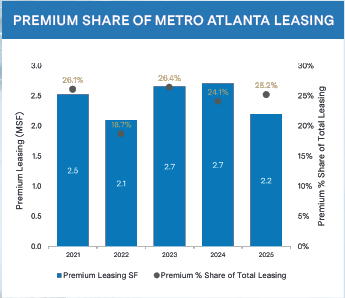

While premium buildings accounted for 17.5% of Metro Atlanta’s total office inventory, they comprised 25.2% of total leasing activity in 2025, above the five-year average of 24.1%. Premium leasing activity in the CBD during 2025 was bolstered by three transactions exceeding 100,000 sq. ft., including Kilpatrick Townsend’s 148,112-sq.-ft.renewal at 1100 Peachtree, Greenberg Traurig LLP’s 110,374-sq.-ft. renewal at Terminus 200, and EY’s 102,195-sq.- ft. new lease at Spring Quarter. EY is relocating from 55 Allen Plaza, part of a wave of tenants migrating from Downtown to Midtown in favor of higher-quality office product.

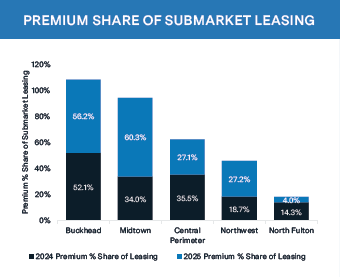

Demand for premium buildings continued to grow across Atlanta’s CBD last year. In Midtown, premium product captured a metro-leading 60.3% share of the submarket’s total leasing activity in 2025, up sharply from 34.0% one year earlier. Buckhead premium space accounted for 56.2% of the submarket’s leasing in 2025—above the 52.1% share recorded in 2024. The Northwest submarket posted meaningful gains as premium product represented 27.2% of total leasing activity in 2025, up from 18.7% the prior year. However, premium leasing

activity softened in Central Perimeter and North Fulton, reflecting a shortage of mid to large block availabilities.

NEW OFFICE DELIVERIES AND OCCUPANCY

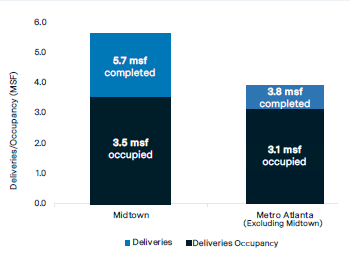

Midtown has been the epicenter of new construction in Metro Atlanta, accounting for 60.2%, or 5.7 million sq. ft., of all new office space built in the region since 2021. Nearly 62.0% of Midtown product built in that time is currently occupied – below the 81.2% occupancy rate across 3.8 million sq. ft. of new buildings built outside of Midtown since 2021. Nearly 33.0% of Midtown’s vacant new-construction space is clustered in West Midtown, where 713,903 sq. ft. of office product delivered since 2021 has yet to be absorbed—highlighting a clear divergence in performance within the submarket.

With limited new construction underway, high-quality space outside the urban core is becoming increasingly scarce.

Outlook

As available premium space tightens and the development pipeline remains historically constrained, vacancy within premium assets is expected to compress further in the coming years. This imbalance between demand and supply will place continued upward pressure on rents, reinforcing premium buildings’ pricing power and widening the performance gap relative to non-premium assets. In an environment defined by muted development and evolving workplace expectations, premium office product is positioned to remain the clear beneficiary of Atlanta’s next phase of market growth.

Alex Kaplan

Senior Vice President of Research

[email protected]

tel 404 595 0500