Market Edge: Texas Grocery Wars – Market Trends 2025–2027

The Accelerating Bifurcation The Texas grocery sector remains in flux following the December 2024 blockage of the $24.6 billion Kroger-Albertsons merger by federal and state regulators. This decision, upheld on antitrust grounds despite proposed divestitures to C&S Wholesale Grocers, has accelerated a “great decoupling” where legacy grocers like Kroger (operating as Kroger) and Albertsons (under banners like Tom Thumb and Randalls) face mounting pressures from regional powerhouses such as H-E-B and national discounters like Walmart and Costco. In 2025, this manifested in targeted closures of underperforming stores, efficiency drives, and a pivot toward specialty and ethnic grocers filling market voids.

Entering 2026, the landscape is bifurcating into “experience giants” (H-E-B, Costco, Central Market) dominating everyday shopping and “cultural specialists” (H Mart, India Bazaar, Enson Market) capturing niche demographics in high-growth areas. Population booms in major markets—Austin, Dallas-Fort Worth (DFW), Houston, and San Antonio—fuel this evolution, with grocery-anchored developments driving record retail occupancy (95.3% in DFW in 2025, projected to rise to 95.4% in 2026).

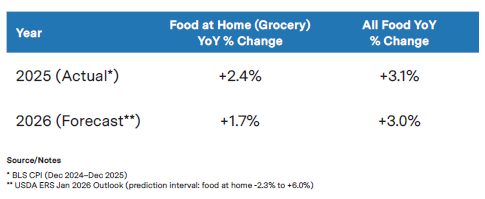

Food prices rose moderately in 2025, with grocery (food-at-home) inflation at 2.4% year-over-year through December, and all food at 3.1%. Forecasts for 2026 show continued pressure but some moderation in groceries:

This ongoing elevation in costs—particularly for everyday staples—continues to push value-conscious consumers toward private labels, discounters, and experiential/ethnic formats that offer perceived better value or cultural appeal. Closures continue, but rapid backfilling by fitness centers, medical facilities, and emerging grocers like Enson Market highlights adaptive reuse trends. By 2027, expect further consolidation among mid-market players, with specialty surges reshaping urban and suburban retail.

The Blocked Merger: Lingering Impacts and Strategic Pivots The FTC’s successful challenge to the Kroger-Albertsons merger, citing insufficient competition safeguards, ended a period of stasis and forced both companies into independent survival modes. Kroger and Albertsons argued the deal was essential to counter Walmart (22% market share) and Costco, but regulators deemed the 579-store divestiture inadequate due to C&S’s limited retail expertise.

- Fallout and Litigation: Albertsons terminated the agreement on December 11, 2024, leading to ongoing lawsuits. In 2025, both pivoted to cost-cutting: Albertsons targeted $1.5 billion in savings over three years, while Kroger merged its Dallas and Houston divisions into a single “Texas Division” in July 2025 to reduce overhead.

- Technology Shifts: Kroger closed several automated fulfillment centers in 2025, retreating from high-tech models to prioritize in-store profitability.

- Market-Wide Effects: The failed merger exposed vulnerabilities in overlapping markets, accelerating closures where H-E-B’s “Marketplace” flagships dominate within 5-mile radii. This “H-E-B Effect” is pronounced in suburban DFW and Houston, where private-label strength and experiential shopping erode legacy shares.

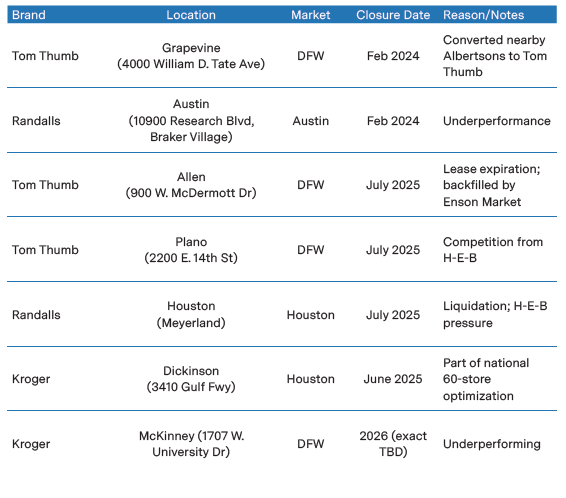

Closures: The Legacy Retreat Accelerates Post-merger blockage, 2025 saw a wave of closures as legacy grocers optimized portfolios amid competitive pressures from H-E-B, Walmart, and Sprouts. Kroger announced 60 national closures in June 2025, extending into 2026, with Texas locations including Dickinson (closed June 2025) and McKinney (1707 W. University Drive). Albertsons’ banners, Tom Thumb and Randalls, continued shrinking, focusing on underperforming sites in high-competition zones.

The table below tracks confirmed closures in major Texas markets from 2024–2026, based on WARN notices, lease expirations, and performance reviews:

- Patterns: Closures cluster in suburban areas with recent H-E-B openings, such as Plano and Allen in DFW. In Houston, Randalls’ footprint dropped from 51 stores in 2005 to 17 by 2020, with further reductions expected in 2026. San Antonio sees minimal legacy closures due to H-E-B’s dominance, while Austin’s competitive mix pressures Randalls.

- At-Risk Stores for 2026: From the blocked divestiture list, vulnerable sites include Tom Thumb in Frisco (5550 FM 423), McKinney (6800 W. Virginia Pkwy), and Randalls in Houston (14610 Memorial Dr) and Galveston (2931 Central City Blvd). Monitor H-E-B expansions for triggers.

Openings and Expansions: The Growth Offensive Grocery development surges in 2025–2026, with H-E-B leading amid Texas’ population growth (projected to hit 32.5 million by 2030). DFW emerges as the nation’s top retail construction market with 7.6 million sq. ft. in the pipeline, driven by grocers. In 2025, 18 new stores opened statewide after seven in 2024; 34 more are slated for 2026–2027.

Key openings by market:

- DFW: H-E-B’s aggressive push includes Euless (opening May 2026, 126,196 sq. ft. at Cheek-Sparger Rd and Rio Grande Blvd), Forney (early 2026), Mid-Cities (2026), Murphy (2026), and potential Dallas city limits (Hillcrest & LBJ, late 2026). Trader Joe’s expands in Bee Cave and Leander; Sprouts opens in The Woodlands (Aug 2025).

- Austin: Aldi opens in Cedar Park (850 N. Bell Blvd, Feb 2026, 23,606 sq. ft.). H-E-B plans Manor (late 2025), Georgetown (late 2025), San Marcos (2026), and East Austin (late 2027).

- Houston: H-E-B’s Jordan Ranch in Katy (Oct 2025, 133,000 sq. ft.) marks its 97th regional store; more in Forney and Mid-Cities (2026). Trader Joe’s in Kingwood (Sep 2025).

- San Antonio: H-E-B opened at 15489 Culebra Rd (Jan 7, 2026, 126,196 sq. ft.); additional sites in Alamo Ranch and tourism-driven areas.

H-E-B’s North Texas expansion enters its most aggressive phase, targeting suburban corridors like US-380.

The Specialty Surge: Cultural Anchors and Ethnic Grocers As mid-market grocers retreat, specialty players fill voids, becoming anchors for mixed-use developments. This “K-Wave” and “Millennial Pivot” targets growing Asian-American and South Asian demographics in tech corridors.

- H Mart: Dallas flagship (Oct 2025, 142,000 sq. ft. on Harry Hines Blvd) transforms Koreatown; Austin second location (late 2025); Haltom City (2026).

- India Bazaar: Allen flagship at The Avenue (SH 121 & Alma, 2026), focusing on organic, health-conscious staples for Collin County tech workers.

- Enson Market: Asian-focused chain enters Texas with Allen (900 W. McDermott Dr, coming soon, backfilling closed Tom Thumb); additional Houston (5708 S. Gessner Rd) and Austin (12815 N Interstate 35) sites planned. Enson specializes in fresh produce, specialty meats, seafood, and amenities like boba tea.

- Market Trends: Ethnic grocers drive experiential retail, with 72% of shoppers citing value in private labels. In 2026, expect more “recession-proof” anchors like H Mart in DFW mixed-use projects.

Second-Generation Reuse: From Groceries to Social Hubs Vacant legacy spaces (20,000–50,000 sq. ft.) are repurposed rapidly:

- Med-Tail and Fitness: Former sites convert to clinics or gyms (e.g., Crunch Fitness in Rowlett, EoS in Dallas, late 2025).

- Pickleball Effect: Indoor facilities like The Picklr (Arlington, Aug 2025) compete for anchors.

- Market Impact: High demand ensures low vacancies (DFW at 5.1%, Austin at 3.4%, Houston at 5.5%, San Antonio at 4.1%).

Looking Ahead

A New Tiered Ecosystem By 2027, Texas’ grocery wars will solidify a tiered system: experience giants for mass appeal, cultural specialists for niches, and shrinking mid-market legacies. DFW leads in growth, followed by Austin’s tech-fueled surge, Houston’s consolidation, and San Antonio’s H-E-B stronghold. Retail owners should monitor WARN notices, lease expirations, and H-E-B expansions. For consumers, this means more options but sustained pressure from food costs (with groceries moderating to +1.7% in 2026 forecasts); for retailers, innovation in value, personalization, and omnichannel is key to survival.

Steve Triolet

Senior Vice President of Research and Market Forecasting

[email protected]

tel 214 223 4008