Houston Retail Market Remains Balanced with Low Vacancy and Active Leasing

EXECUTIVE SUMMARY

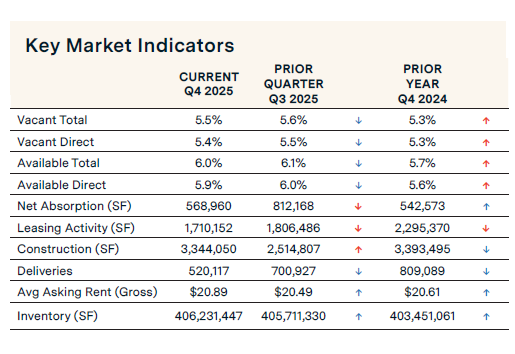

The Houston retail market remained balanced in Q4 2025, with a healthy vacancy rate of 5.5%. This stability is attributed to the balance between supply and demand, as net absorption for the quarter came in at 568,960 square feet, and the addition of 520,117 square feet of new construction was added to inventory. Leasing activity remained brisk, with only a 5.3% decline over the quarter. The construction pipeline increased 33%, with 3.3 million square feet under construction. Meanwhile, the average asking rental rate continued to increase, up 2.0% quarterly to $20.89 per square foot.

Houston Economic Update

Houston’s unemployment rate increased from 4.5% in July to 4.8% in September, and increased from 4.4% one year ago. Houston’s labor market recorded employment growth of 0.9% year-over-year (ending September 2025), adding 30.700 jobs, a decrease compared to the annual 66,700 jobs gained in September a year ago.

Job growth was uneven across sectors. Education and Health Services employment was a standout, growing at an annualized rate of 3.3% from September 2024 to September 2025 (15,100 jobs). Additional sectors showing resilience include Mining and Logging, which expanded at a 2.9% annualized rate (2,300 jobs), and the Leisure and Hospitality sector, which increased at a 2.5% annualized rate (9,000 jobs). Sectors that experienced job losses include Information, down 2.7% (700 jobs); Professional and Business Services, down 2.4% (13,700 jobs); and Manufacturing, down 0.8% (1,900 jobs).

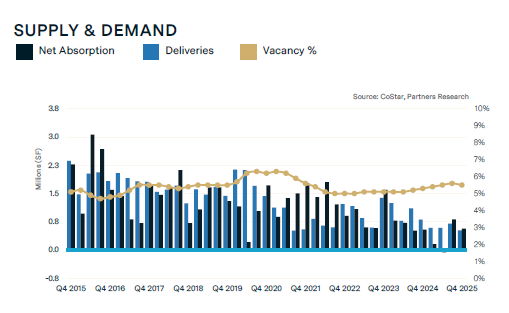

SUPPLY & DEMAND

KEY MARKET INDICATORS

MARKET OVERVIEW

Vacancy Remains Low at 5.5%

The total average vacancy rate fell 10 basis points over the quarter to 5.6%, but was up 20 basis points year over year. Over recent quarters, supply and demand have been in lockstep, with most of the net absorption going into new deliveries. The total availability rate dropped from 6.1% to 6.0% on a quarterly basis but increased by 30 basis points from Q4 2024. If supply and demand continue to mirror each other, vacancy will remain tight in the near term.

Positive Demand Decreases, but In Step with Deliveries

Net absorption, which is the difference between move-ins and move-outs, decreased from the previous quarter, recording 568,960 sq. ft., pushing the year-end total net absorption to 1.8 million sq. ft. Although absorption declined, it was offset by new deliveries, helping keep vacancy low. Notable Q4 2025 move-ins include EOS Fitness moving into 50,000 sq. ft. at 9025 Highway 6 South in the Sugar Land submarket, Havertys Furniture moving into 42,000 sq. ft. in Valley Ranch Town Center in New Caney, and AR’s Entertainment Hub moving into 40,000 sq. ft. in Spring Park Village.

Leasing Activity Down, but Still Healthy

Although leasing activity declined 5.3% during Q4 2025, 1.7 million sq. ft is still a healthy quarterly total for the tight Houston market, which helped push the year-end leasing total to over 8.0 million sq. ft. Recently signed leases included DICK’s Sporting Goods’ 60,000 sq. ft. lease at The Grand at Aliana shopping center, TakeOff Adventure Park’s 60,000 sq. ft. lease at Fairmont Parkway shopping center, Floor and Décor Outlets’ 56,000 sq. ft. lease at Meyer Park shopping center, and Charlie’s Collectible Show’s 44,000 sq. ft. lease at Legacy Pointe.

Deliveries Decreased, While the Construction Pipeline Increased

Construction deliveries were down 25.8% for the quarter, adding 520,117 sq. ft. Deliveries were down 35.7% for the year. The construction pipeline stands at 3.3 million sq. ft., up 33% quarter-over-quarter but down 1.5% year-over-year. Much of the construction is in the Northwest and Southwest submarkets, near recently developed residential subdivisions.

Investment Sales Trends

According to CoStar Capital Market Analytics, the cumulative 12-month sales volume at the end of the fourth quarter in the Houston retail market was $841 million. With 910 deals completed, the average transaction price currently stands at $268 per sq. ft., and the average capitalization rate is 7.1%. Notable sale transactions in Q4 2025 include the 190,510 sq. ft. Baybrook Village (part of a portfolio), purchased by Fidelis Realty Partners from O’Connor Capital Partners for an undisclosed amount. Also, Unilev Capital Corporation’s 419,731 sq. ft. West Road Plaza is currently under contract, and the price is undisclosed.

Rental Rates Continue Upward Climb

Balanced demand and activity have kept Houston’s retail vacancy low, which, in turn, has kept the average asking rent on an upward trend toward record highs. The average NNN rental rate marginally rose 2.0% over the quarter from $20.49 per sq. ft. to $20.89 per sq. ft. in Q4 2025. Year-over-year, the metro’s average asking rent increased 1.4% from $20.61 per sq. ft. At the submarket level, the Inner Loop submarket continues to have the highest average rate at $30.44 per sq. ft. In contrast, the Southeast submarket had the lowest average rate at $17.51 per sq. ft.

For More Information, Contact:

Steve Triolet

SVP of Research and Market Forecasting

tel 214 223 4008

[email protected]