DFW Office Market Activity Slows Down in Q4 2025

EXECUTIVE SUMMARY

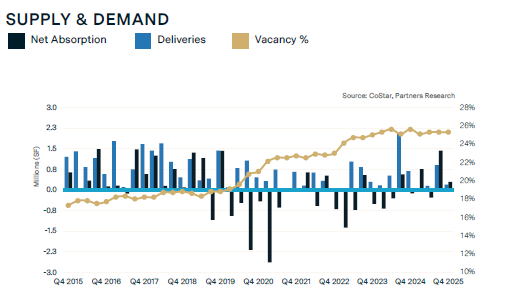

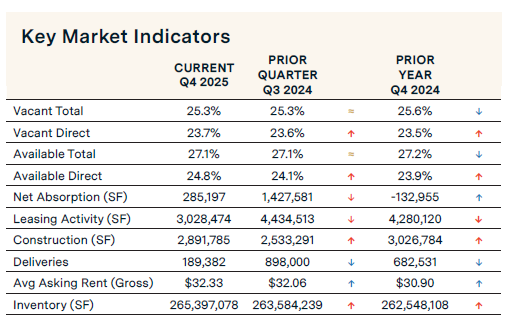

Momentum slowed between quarters in the Dallas-Fort Worth office market. Leasing activity decreased 31.7% quarterly from 4.4 million sq. ft. to 3.0 million sq. ft. Total net absorption saw a significant drop for the quarter, decreasing 80.0% from 1.4 million sq. ft. in Q3 to 285,197 sq. ft. in Q4 2025. Class A properties recorded positive absorption while Class B properties posted negative absorption. Due to the slowdown in deliveries and Class A positive absorption, the vacancy rate remained unchanged at 25.3%.

Construction deliveries for the quarter totaled 189,382 sq. ft., down significantly from the previous quarter, and the construction pipeline increased 14.2% over the quarter to 2.9 million sq. ft. Rental rates rose 2.5% over the quarter and 4.8% over the year to $32.06 per sq. ft. Class A gross rental rates rose again to a record high of $36.20 per sq. ft. and are forecasted to continue to rise. Class B rental rates increased to $25.58 per sq. ft. from $25.22 per sq. ft. in Q3 2025.

SUPPLY & DEMAND

KEY MARKET INDICATORS

MARKET OVERVIEW

Dallas Economic Update

Employment in DFW grew at an annualized rate of 0.8% in September, adding 34,100 jobs annually, while Texas employment increased by 1.2%. The unemployment rate dropped 20 basis points to 4.2% from 4.4% in August. The jobless rate was 4.2% in Dallas and 4.1% in Fort Worth. The most significant gains were in mining, logging and construction, leisure and hospitality, government, and education and health services sectors. The largest losses were in manufacturing, transportation and utilities, and professional and business services.

Vacancy Rate Remains at 25.3%

The total vacancy rate remained unchanged between quarters at 25.3% and dropped 30 basis points over the year. Submarkets with generally older inventory, such as the Dallas CBD at 33% and Far North Dallas and Las Colinas at 31%, are affected. The higher vacancy rates are primarily due to tenants gravitating toward newer properties with more amenities, which are more highly concentrated in Uptown and other northern suburban submarkets.

Construction Pipeline Increases, Delivers Decrease

Construction deliveries for the quarter totaled 189,382 sq. ft., a 78.9% decrease from the previous quarter. The under-construction pipeline grew by 14.2% over the quarter to 2.9 million sq. ft. Most of the pipeline is in the Uptown/Turtle Creek submarket (45%), followed by the Far North Dallas submarket (26.8%), with the remainder sprinkled across the other submarkets.

Leasing Activity Decreased Quarterly and Annually

Quarterly leasing velocity, which is comprised of both new leases and renewals, stood at 3.0 million sq. ft. during Q4 2025, a 31.7% decrease over last quarter and down 29.2% from Q4 2024. Notable lease transactions in Q4 2025 include Fujitsu’s 70,000 sq. ft. lease at Galatyn Commons C in Richardson, Unleashed Brands’ 51,000 sq. ft. lease in 600 ELC, and Newrez’s 47,000 sq. ft. lease at Cypress Waters in Coppell.

Net Absorption Positive, But Experiences a Sharp Drop Over the Quarter

Net absorption—move-ins minus move-outs—was positive 285,197 sq. ft. in Q4 2025, sharply down 80% quarter over quarter. Only Class A properties contributed to positive absorption, with Class A recording 310,702 sq. ft. Class B posted -25,505 sq. ft. of negative net absorption in Q4 2025. Some tenants that moved in during Q4 2025 included State Farm, which moved into 426,000 sq. ft. at Four CityLine, and GEICO, which took 165,000 sq. ft. at Galatyn Commons B.

Investment Sales Trends

CoStar Capital Market Analytics reports the cumulative 12-month sales volume at $1.3 billion in the DFW office market. With 204 deals completed, the average transaction price currently stands at $286 per sq. ft. with an average cap rate of 7.9%. Notable recent sale transactions in Q4 2025 include Crescent Real Estate LLC’s purchase of 2100 McKinney from MetLife Investment Management for a reported price of $218 million or $604 per sq. ft. The 360,860 sq. ft. property is 81% leased. Also, Real Capital Solutions, Inc. purchased the 464,290 sq. ft. Walnut Glen Tower from Intercontinental Real Estate Corporation for $26.1 million or $56.21 per sq. ft. The property, located in the Central Expressway submarket, is 76.8% leased.

Rental Rates Continue to Rise

The average gross rental rate for the DFW office market is $32.33 per sq. ft., up 0.8% quarterly from $32.06 per sq. ft., and up 4.6% annually. The Uptown/Turtle Creek submarket boasts the highest rental rates, with the overall average gross rent currently sitting at $62.10 per sq. ft. The lowest rental rate in the Stemmons Freeway submarket is $21.46 per sq. ft.

For More Information, Contact:

Steve Triolet

SVP of Research and Market Forecasting

tel 214 223 4008

[email protected]