Year-end Surge in Positive Absorption Keeps DFW Retail Market Vacancy Low

EXECUTIVE SUMMARY

The Dallas-Fort Worth (DFW) retail market experienced a surge in positive net absorption in Q4 2025, helping keep the vacancy rate low at 5.1%, despite an increase in deliveries. The under-construction pipeline rose 6.1% quarter over quarter to 7.4 million sq. ft., which is 82% pre-leased. Most of the construction underway is concentrated in the northern and southwestern submarkets of Dallas, aligning with housing growth. Average asking rates jumped 16.8% quarter-over-quarter and 22.6% year-over-year to $24.07 per sq. ft. Central Dallas, East, and North Central Dallas continue to command premium rents, while Central Fort Worth and Southwest Dallas offer more affordable options. Overall, the DFW retail market exhibits a healthy balance of demand, investment, and growth opportunities, driven by strong market fundamentals.

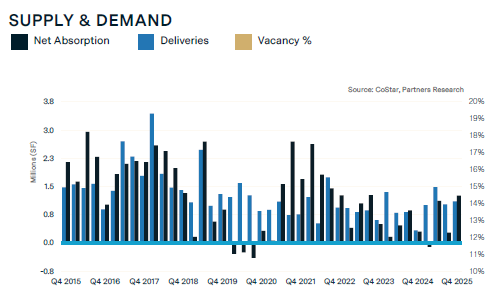

SUPPLY & DEMAND

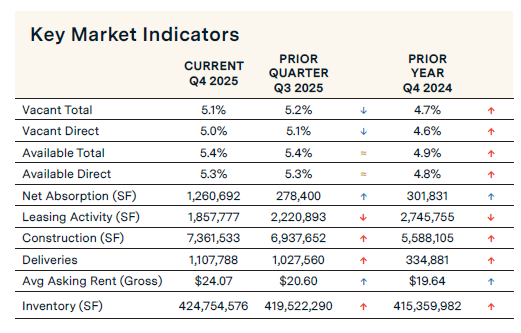

KEY MARKET INDICATORS

MARKET OVERVIEW

Dallas Economic Update

Employment in DFW grew at an annualized rate of 0.8% in September, adding 34,100 jobs annually, while Texas employment increased by 1.2%. The unemployment rate dropped 20 basis points to 4.2% from 4.4% in August. The jobless rate was 4.2% in Dallas and 4.1% in Fort Worth. The most significant gains were in mining, logging and construction, leisure and hospitality, government, and education and health services sectors. The largest losses were in manufacturing, transportation and utilities, and professional and business services.

Vacancy Inches Down 10 Basis Points

The overall vacancy rate in the DFW retail market decreased by 10 basis points over the quarter but rose by 40 basis points annually to 5.1%. This small quarterly decrease is most likely due to increased absorption, muted by quarterly deliveries that are not fully pre-leased. The vacancy rate is still low compared to the historical highs of 9.0% to 10.0% in 2009 through 2013.

Net Absorption Sharply Increases

Net absorption, calculated as move-ins minus move-outs, is at 1,260,692 sq. ft., sharply up from the previous quarter. Submarkets contributing to the positive absorption include East Dallas Outlying, Far North Dallas, North Central Dallas, and Southeast Dallas. Some of the notable moves during Q4 2025 include Target’s move into 148,000 sq. ft. at Rayzor Ranch Town Center, Lowe’s taking 124,000 sq. ft. at 634 W Interstate 30 in Royse City, and Kroger moving into 122,000 sq. ft. at Bonds Ranch Marketplace in Ft. Worth. The Southwest Dallas submarket recorded the highest amount of negative absorption in Q4 2025.

Leasing Activity Drops Quarterly and Annually

Leasing activity decreased 16.3% over the quarter, but remained healthy at 1.9 million sq. ft. Some of the more notable transactions in Q4 2025 include Club 4 Fitness’s lease for 59,000 sq. ft. at 14th Street Market in Plano, Belk’s lease for 38,000 sq. ft. at Preston Ridge shopping center, and Padel Haus’s lease for 25,000 sq. ft. at 1500 Dragon St.

Deliveries and Construction Pipeline Increase

Construction deliveries were up over the past quarter by 7.8% from 1.0 million sq. ft. in Q3 2025 to 1.1 million sq. ft and up 231% from 334,881 sq. ft. delivered one year ago. The under-construction pipeline increased 6.1% quarterly and 31.7% annually to 7.4 million sq. ft. Far North Dallas, North Central Dallas, and Suburban Fort Worth submarkets have the highest levels of construction currently underway, with 1.7 million sq. ft., 1.6 million sq. ft., and 1.2 million sq. ft., respectively. Two of the largest centers under construction are Field West in Frisco (350,000 sq. ft.) and 2209 East University Drive in Denton (340,000 sq. ft.)

INVESTMENT SALES TRENDS

CoStar Capital Market Analytics reports that the cumulative 12-month sales volume in the DFW retail market is $1.2 billion. With 842 deals completed, the average transaction price currently stands at $321 per sq. ft. with an average cap rate of 6.9%. Notable sale transactions in Q4 2025 include Albanese Cormier Holdings, LLC’s purchase of the 252,000 square foot Shops at Legacy North for an undisclosed amount from CTO Realty Growth Inc. Additionally, the 161,000 square foot Wedgewood Village was purchased by H & R Sai Investment. Both sales were part of larger investment portfolios.

Rental Rates Jump 16.8%

Average asking rental rates jumped 16.8% quarter-over-quarter and 22.6% year-over-year to $24.07 per sq. ft. The submarkets with the highest rental rates include North Central Dallas ($29.31 per sq. ft.), East Dallas Outlying ($28.89 per sq. ft.), and Central Dallas ($27.59 per sq. ft.), which are well above the metro average. In contrast, the lowest-asking-rent submarkets include Southwest Dallas ($16.18 per sq. ft.), Central Fort Worth ($17.28 per sq. ft.), and Southeast Dallas ($17.40 per sq. ft.).

For More Information, Contact:

Steve Triolet

SVP of Research and Market Forecasting

tel 214 223 4008

[email protected]