DFW Industrial Market Recorded a Significant Increase in Absorption and Leasing Activity Over the Quarter

EXECUTIVE SUMMARY

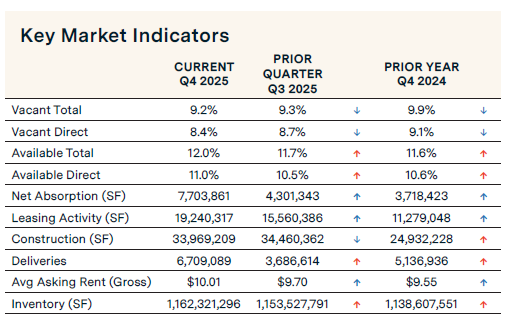

The Dallas-Fort Worth (DFW) industrial market experienced increased absorption and leasing activity; however, vacancy only decreased by 10 basis points due to increased deliveries.

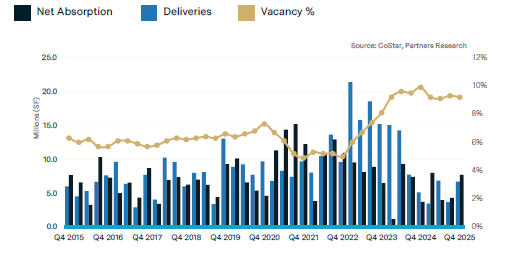

Deliveries totaled 6.7 million square feet this quarter, a sharp 82% increase from the previous quarter and 30.6% from the previous year. Construction activity slightly decreased 1.4% over the quarter to 34 million square feet.

Leasing activity increased by 23.6% over the quarter and by 70.6% year-over-year. Quarterly net absorption increased significantly by 79.1% to 7.7 million square feet, primarily driven by warehouse/distribution properties, which recorded 7.6 million sq. ft. The manufacturing segment recorded negative absorption of -121,430 sq. ft., while Flex posted positive net absorption totaling 231,896 sq. ft.

Investment sales totaled $2.4 billion over the past year, with 968 properties sold at an average sales price of $129 per sq. ft. and an average cap rate of 6.4%.

Rental rates were up 3.2% for the quarter and up 4.8% year-over-year to an average of $10.01 per square foot. The market’s shift toward normalization reflects a recalibration after years of extraordinary growth, signaling a steady foundation for future activity.

SUPPLY & DEMAND

KEY MARKET INDICATORS

DFW ECONOMIC UPDATE

Employment in DFW grew at an annualized rate of 0.8% in September, adding 34,100 jobs annually, while Texas employment increased by 1.2%. The unemployment rate dropped 20 basis points to 4.2% from 4.4% in August. The jobless rate was 4.2% in Dallas and 4.1% in Fort Worth. The most significant gains were in mining, logging and construction, leisure and hospitality, government, and education and health services sectors. The largest losses were in manufacturing, transportation and utilities, and professional and business services.

MARKET OVERVIEW

Vacancy Rate Drops 10 Basis Points to 9.2% Over the Quarter

The overall vacancy rate in DFW’s industrial market dropped 10 basis points to 9.2% over the quarter and decreased 70 basis points from 9.9% recorded one year ago. For the different industrial property types, the total vacancy rates are 6.6% for Flex, 4.2% for Manufacturing, and 10.1% for Warehouse/Distribution space. DFW’s industrial market is currently categorized as having “neutral conditions”—with a vacancy rate between 8% and 10%—meaning neither landlords nor tenants have a significant upper hand in overall lease negotiations.

Deliveries Up, Construction Down

Deliveries in the DFW industrial market increased significantly to 6.7 million sq. ft. from 3.7 million sq. ft., down 82% from the previous quarter and down 30.6% year-over-year. The under-construction pipeline dropped marginally by 1.4% quarter over quarter but rose 36.2% year over year.

Leasing up 23.6% from the Previous Quarter

Leasing activity has increased by 23.6% over the past quarter and by 70.6% over the year, as new construction entering the market has returned to historic norms. Recent notable lease transactions include Moonshot signing a lease for 505,000 sq. ft. at Lewisville 121 Business Center, Thrive Market signing a lease for 378,000 sq. ft. at DFW Commerce Center, and Irby signing a lease for 307,000 sq. ft. at Crossroads Logistics Park.

Quarterly Positive Net Absorption Increases 79.1% to 7.7 million sq. ft.

Net absorption—move-ins minus move-outs—recorded 7.7 million sq. ft. in Q4 2025, pushing the year-end total net absorption to 26.4 million sq. ft. Warehouse/distribution properties accounted for most of the positive net absorption for the quarter, with 7.8 million sq. ft. recorded, while flex recorded 231,896 sq. ft. Manufacturing reported negative absorption of -121,430 sq. ft. in the fourth quarter. Notable recent move-ins include Hayes Company taking 1.5 million sq. ft. in Gateway Crossing Logistics Park, Modine moving into 684,000 sq. ft. in Wildlife Commerce Park, Maersk taking 348,000 sq. ft. in Cedar Hill Logistics Center, and SPM Oil & Gas taking 305,000 sq. ft. at Northlink C.

Investment Sales Trends

CoStar Capital Market Analytics reports that over the past 12 months, sales volume for the DFW market totaled $2.4 billion. This represents 968 properties sold with an average sales price of $129 per sq. ft. and an average cap rate of 6.4%. Notable recent sales transactions include EQT Real Estate’s disposition of the 796,000-square-foot Speedway Logistics Crossing Building 3 to Sterling Investors for $83.5 million, or $105 per sq. ft. Also, LaSalle Investment Management purchased the 1650 Lakeside Parkway as part of a larger portfolio from QuadReal. The property contains 292,850 sq. ft. and was 49% leased at the time of sale.

Asking Rents at an All-Time High of $10.01 per sq. ft. Annually

The average monthly rental rate for the DFW industrial market was $10.01 per sq. ft., up 3.2% from $9.70 in Q3 2025 and up 4.8% year-over-year from $9.55 per sq. ft. The average monthly rate for flex space stood at $13.79 per sq. ft., while the rates for manufacturing space and warehouse/distribution space were $6.75 per sq. ft. and $9.33 per sq. ft., respectively.The Northwest Dallas Outlying and DFW Airport submarkets currently have the highest overall average rates at $19.13 and $12.87 per sq. ft., respectively.

For More Information, Contact:

Steve Triolet

SVP of Research and Market Forecasting

tel 214 223 4008

[email protected]