Atlanta Retail Market Showed Mixed Results

EXECUTIVE SUMMARY

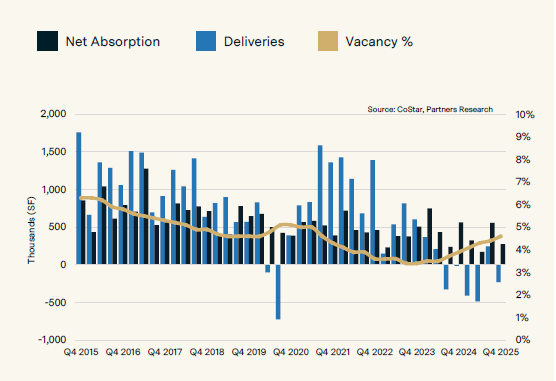

While healthy population and household wage growth in Metro Atlanta continued to bolster consumption of goods, total annual leasing in 2025 declined by 14.4% year-over-year (YOY) to 5.8 million sq. ft. Leasing activity moderated amid heightened macroeconomic uncertainty and limited availability, evidenced by a 4.6% vacancy rate in Q4. However, vacancy trended upward at a measured pace in the six preceding quarters (Q2 2024 – Q3 2025), providing much-needed supply-side relief. Closures by major retailers increased vacancy levels while simultaneously weighing on overall occupancy. Atlanta recorded 228,770 sq. ft. of negative net absorption in the fourth quarter, bringing total occupancy loss for the year to 874,556 sq. ft. Despite the decline, rental rate momentum remained intact, with average triple-net rents across Atlanta rising by 4.1% quarter-over-quarter (QOQ) to a record $19.98 per sq. ft., reflecting broad-based market health.

A slowdown in new construction placed upward pressure on rents as elevated construction and financing costs continued to suppress development. Atlanta welcomed 1.3 million sq. ft. of new product in 2025, a 33.0% drop from 2024. Most submarkets recorded a drop-off in retail construction, with steep declines seen in Airport/South Atlanta, Buckhead, and Central Perimeter. The construction pipeline also thinned, with only 837,139 sq. ft. of space under construction in the fourth quarter, the lowest level since Q1 2010.

SUPPLY & DEMAND

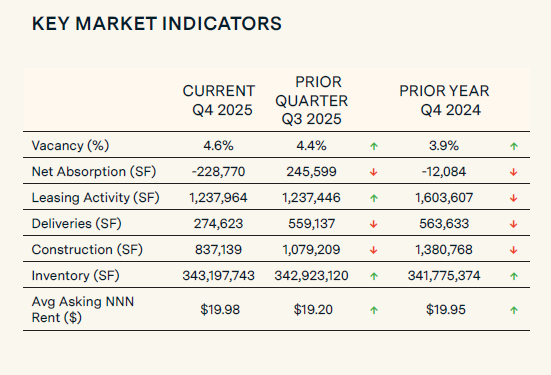

KEY MARKET INDICATORS

MARKET OVERVIEW

ATLANTA ECONOMIC UPDATE

Payroll growth in the Atlanta Metro increased by a modest 0.3% YOY in November, a notable deceleration from year-ago levels amid ongoing job loss in the construction sector (-2.7%). Construction employment has softened in response to still elevated financing costs that contributed to fewer new project starts in the office, retail and industrial sectors. However, the labor market sustained positive momentum in other industries as robust payroll growth persisted in education and health services (4.7%) and leisure and hospitality (2.9%). Atlanta’s economic fundamentals continued to benefit from sustained population growth as the region added over 64,000 residents between 2024 and 2025. Strong in-migration and the subsequent expansion of the region’s consumer base reinforced the metro’s appeal to companies seeking access to a deep, educated workforce, further supported by favorable tax incentives and a business-friendly regulatory environment.

RETAIL MARKET REMAINED RESILIENT DESPITE SOFTENING COMMUNITY CENTER DEMAND

The slowdown in leasing activity during 2025 reflected a notable pullback in occupier demand for community centers, which documented a 36.1% YOY drop in leasing to 851,174 sq. ft. However, overall retail market fundamentals remained healthy in 2025, with power centers standing out as a key source of demand. Total leasing activity for the product type reached a three-year high of 531,983 sq. ft., reflecting a 16.6% increase from 2024. Moreover, leasing in lifestyle centers reached a four-year high of 237,906 sf in 2025, up 43.8% versus the prior year. On the submarket level, tenant demand was pronounced in the Midtown/Downtown submarket, where transactions climbed 42.6% to 323,415 sq. ft. Powering the increase was the 150,000-sq.-ft. Wayfair lease at The District At Howell Mill and the 49,538-sq.-ft. Publix deal at Summerhill Station. The Centennial Yards project taking shape Downtown has also welcomed a growing roster of retail tenants, including Shake Shack, SKOL Brewing, Café Momentum, and Brown Toy Box, just to name a few. Occupier demand is projected to improve across Metro Atlanta next year, as sustained population growth and income gains reinforce the region’s long-term demand drivers.

NORTHEAST SUBMARKET DEFIED REGIONAL CONSTRUCTION SLOWDOWN

Despite stable occupier demand, retail construction activity hovered near historic lows in 2025. The muted development pipeline–driven by a declaration in new construction south of Atlanta–highlighted the impact that high construction costs and restrictive financing conditions had on new supply. However, the Northeast proved largely insulated from the slowdown affecting other parts of Atlanta. Deliveries in the submarket increased by 34.0% YOY to 714,589 sq. ft. as developers increasingly targeted high population growth areas in Barrow, Jackson, and Hall counties. The Northeast also boasted the most under construction product at 243,759 sq. ft., which represented 29.1% of the total Metro Atlanta construction pipeline in the fourth quarter.

HEALTHY INVESTOR DEMAND PERSISTED

Investor appetite remained strong in 2025 as $2.4 billion of retail sales were recorded in 2025 across 714 properties. The average cap rate remained firm at 7.3% in 2025, while the retail sale price per sq. ft. increased by 4.0% YOY to $196.3. Among the most significant trades of Q4 2025, SITE Centers, sold the 356,414-sq.- ft. Perimeter Pointe shopping center in Sandy Springs for $48.0 million, or $134.67 per sq. ft. The property was fully leased at the time of sale and includes national tenants such as LA Fitness, Dick’s Sporting Goods, and Regal Cinemas. Retail investor sentiment is expected to remain positive in 2026, supported by stabilizing financing rates, limited availability, and a new construction pipeline that remains near historic lows.

For More Information, Contact:

Alex Kaplan

SVP of Research

tel 404 850 0667

[email protected]