EXECUTIVE SUMMARY

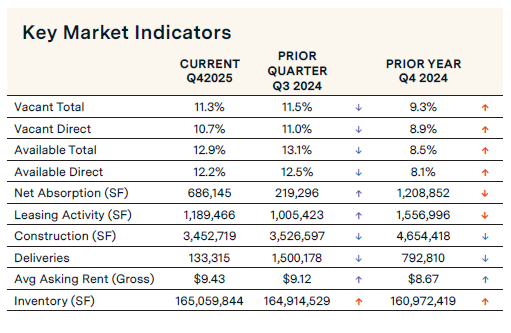

San Antonio’s industrial market posted 686,145 sq. ft. of positive net absorption in Q4, pushing the 2025 year-end total to 1.1 million sq. ft. Construction deliveries decreased 91% over the quarter, which helped contribute to a decrease in the vacancy rate from 11.5% to 11.3%. A significant portion of vacancies, 81%, continues to be carried by the warehouse/distribution sector, which fortunately contributed the most to positive absorption (690,576 sq. ft.) in Q4 2025. Total construction activity slowed by 2.1% over the quarter and by 25.8% over the year. Leasing activity increased, rising 18.3% over the quarter to 1.2 million sq. ft.

SUPPLY & DEMAND

KEY MARKET INDICATORS

MARKET OVERVIEW

SAN ANTONIO ECONOMIC UPDATE

According to the U.S. Bureau of Labor Statistics, the San Antonio unemployment rate increased from 4.1% in August 2025 to 4.2% in September 2025. The unemployment rate in Texas jumped from 4.1% to 4.4% over the same period. San Antonio added 24,200 jobs between September 2024 and September 2025, a 1.8% change. Sectors with the largest annual gains included Education and Health Services at 6.2%, the Trade, Transportation, and Utilities sector at 2.5%, and the Total Private sector at 2.2%. The sector with the highest job losses over the year was the Information sector at -3.5%.

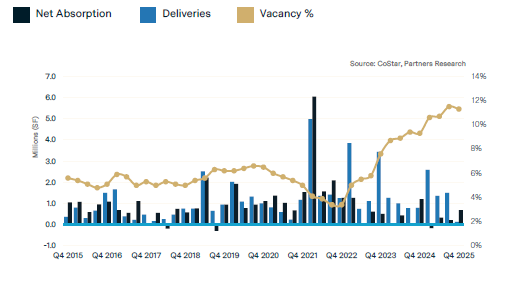

VACANCY EDGES DOWN 20 BASIS POINTS

The overall vacancy rate in San Antonio’s industrial market is 11.3%, down from 11.5% in the previous quarter. Flex, Manufacturing, and Warehouse/Distribution space have vacancy rates of 8.4%, 8.1%, and 12.4%, respectively. Increased quarterly leasing activity and a sharp decrease in new deliveries helped push the vacancy rate down 20 basis points. With 46% of the construction pipeline pre-leased, the total vacancy rate could increase slightly in the short term due to additional new inventory.

NET ABSORPTION INCREASED SHARPLY IN Q4 2025

Net absorption—move-ins minus move-outs—remained positive in Q4 2025, sharply increasing 213% quarterly to 686,145 sq. ft. Warehouse/distribution properties contributed the highest amount of positive absorption in Q4 2025, posting 690,576 sq. ft., followed by Flex (54,161 sq. ft.), while manufacturing recorded negative absorption of 58,592 sq. ft. Recent notable move-ins include QTS Data Centers moving into 366,000 sq. ft. in 8357 Potranco Rd in the Far West submarket, and Microsoft moved into its new 300,000 sq. ft. facility at 3354 FM 471 N. Additionally, CyrusOne occupied 280,000 sq. ft. at 14677 Omicron Dr.

LEASING ACTIVITY INCREASES

Quarterly leasing velocity—comprised of new leases and renewals—stood at 1.2 million sq. ft., up 18.3% from 1.0 million sq. ft. in Q3 2025. The Warehouse/Distribution sector accounted for most of the leasing activity (79%), with more subdued activity in Flex and Manufacturing properties. Recently signed leases included Pathmark’s sublease of 70,000 sq. ft. in Logistics Commerce Center; Pilkinton North America, which signed a 34,000 sq. ft. lease at Gateway 10, Building 2; and Northcuts Wholesale, which signed a 25,000 sq. ft. lease at 3535 N Panam Expressway.

AVERAGE ASKING RENTAL RATES INCREASE

San Antonio’s industrial market average monthly rental rate (NNN) increased 3.4% over the quarter from $9.12 per sq. ft. to a record high of $9.43 per sq. ft. The average monthly rate for Flex Space was $13.85 per square foot, while the rates for Manufacturing and Warehouse/Distribution space were $8.29 and $8.56 per square foot, respectively.

DELIVERIES AND THE CONSTRUCTION PIPELINE DECREASE

Construction deliveries fell sharply by 91% in Q4 2025, with 133,315 sq. ft. completed. The construction pipeline dropped 2.1% over the quarter to 3.45 million sq. ft. Some of the larger projects under construction in Q4 2025 include the 512,000 sq. ft. TriPoint Logistics Center Building 1, located in the Guadalupe County submarket, and a 500,000 sq. ft. building in Medio Creek Business Park in the South submarket.

INVESTMENT SALES TRENDS

CoStar Capital Market Analytics reports a cumulative 12-month sales volume of $96.2 million for 2025. Over the past year, 132 deals were completed in San Antonio’s industrial market with an average transaction price of $81 and an average cap rate of 7.6%. Recent notable sales include Building 1 (560,500 sq. ft.) in the Rosillo Creek Industrial Park, purchased by Amazon from Milam Real Estate Capital LLC for an undisclosed amount. Additionally, Circle Industrial purchased a 395,800 sq. ft. building at the I-35 Logistics Center from Westcore for a reported $45.5 million, or $115 per sq. ft.

For More Information, Contact:

Steve Triolet

SVP of Research and Market Forecasting

tel 214 223 4008

[email protected]