![]()

Part I: Texas Senate Bill 3 – THC Ban Impact Analysis

Texas Senate Bill 3 (SB 3), introduced in the 89th Regular Legislative Session (2025), aimed to prohibit the sale, distribution, and possession of most consumable hemp-derived THC products, including popular items like delta-8 THC, delta-9 THC (beyond trace amounts), and other intoxicating cannabinoids found in vapes, edibles, gummies, and tinctures. The bill targeted products derived from hemp under the 2018 federal Farm Bill, which allows hemp with less than 0.3% delta-9 THC, but sought to close what proponents called a “loophole” allowing intoxicating alternatives to marijuana. Sponsored by Lt. Gov. Dan Patrick and supported by conservative lawmakers, the bill passed both the Texas Senate and House but was vetoed by Gov. Greg Abbott on June 22, 2025. In his veto statement, Abbott argued that the outright ban would face immediate legal challenges under federal law, lead to prolonged lawsuits, and harm small businesses, instead calling for targeted regulations to address safety concerns like child access and product testing.

The veto preserved Texas’s booming hemp industry, which includes retail sales of THC-infused products legal since a 2021 court ruling blocked a state health department ban attempt. However, the issue persists, with ongoing special sessions debating similar measures. This report examines the potential impacts if SB 3 had not been vetoed, the likelihood of similar legislation resurfacing (SB 2024 already placed some restrictions on the industry), and the broader implications for the retail sector, particularly vaping and smoke shops where over half reportedly derive more than half their profits from THC and related products.

Potential Impacts if the Governor Had Not Vetoed SB 3

If SB 3 had become law, it would have effectively dismantled a significant portion of Texas’s hemp-derived cannabinoid market by banning all consumable THC products except those in the state’s limited medical cannabis program (expanded in 2025 to make Texas the 40th state with medical marijuana access). This would have triggered widespread economic fallout, especially in the retail sector, where THC products drive substantial revenue. Key impacts include:

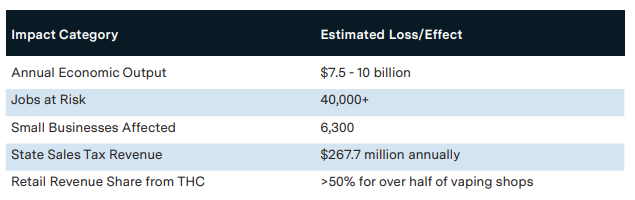

- Economic Losses and Job Destruction: The Texas hemp industry, including cultivation, processing, manufacturing, and retail, generates an estimated $8–10 billion in annual economic output, supporting over 40,000 jobs and contributing $267.7 million in state sales tax revenue. A ban would have eliminated the consumable hemp product market, leading to projected losses of $7.5 billion in industry value and the closure of up to 6,300 small businesses. Farming and processing sectors would suffer reduced demand for hemp crops, while retail outlets would face immediate inventory disposal and revenue drops.

- Retail Sector Devastation, Especially Vaping and Smoke Shops: THC products, particularly delta-8 vapes, edibles, and flower, account for a dominant share of sales in many retail outlets. Industry data indicates that delta-8 sales have spiked sharply, with some retailers reporting 20% of CBD customers shifting to these products. In Texas, where delta-8 remains legal in a gray area, over 11% of surveyed outlets sell delta-8, and 96% of those offer vapes or flower formats. Given that more than half of vaping and related shops derive over half their profits from THC and related items, a ban would force widespread closures or pivots to non-intoxicating alternatives like CBD, which generate lower margins. Retailers have already signaled plans to relocate to other states or sue the state, exacerbating job losses and reducing local tax bases.

- Broader Ripple Effects:

- Consumer and Health Impacts: Users, including veterans relying on these products for pain management, would turn to unregulated black markets, potentially increasing poisonings (calls to Texas poison control centers have risen with delta-8 popularity). The ban could also strain the newly expanded medical cannabis program.

- Legal and Fiscal Costs: Immediate lawsuits would delay enforcement, costing taxpayers in litigation while federal preemption under the Farm Bill remains a hurdle.

- Industry Contraction: Hemp farming profitability would plummet, with processors and manufacturers losing markets for intoxicating extracts.

The following table summarizes key projected economic impacts based on industry analyses:

Likelihood of the Bill Resurfacing and Potential Future Impacts

The likelihood of a similar bill resurfacing is high, driven by persistent conservative pressure despite Gov. Abbott’s preference for regulation over outright bans. After the veto, Abbott called a special session in July 2025 to establish “commonsense THC regulations,” such as age restrictions, testing standards, and limits on potency. However, the Texas Senate, led by Lt. Gov. Patrick (who championed the original ban), ignored this directive and advanced a near-identical THC ban (via bills like SB 5) in the first special session and again in the second special session, which began in August 2025 and remains ongoing as of August 21, 2025. The Senate passed a ban measure on August 18, 2025, fast-tracking it amid debates on other issues like abortion pills and bathroom restrictions. The House has shown bipartisan support for bans in the past, but Democratic returns and industry lobbying may complicate passage.

If no ban passes in upcoming special sessions, the issue is almost certain to return in the 90th Regular Session (2027), as lawmakers have repeatedly attempted to ban delta-8 since 2021, including via health department rules blocked by courts and prior bills. Factors increasing likelihood include public health concerns (e.g., unregulated products leading to poisonings), pressure from medical cannabis advocates who view hemp THC as competition, and conservative opposition to any intoxicating substances outside medical use. However, opposition from veterans, small business owners, and economic analysts could lead to compromise regulations instead.

Potential Future Impacts: If a ban is enacted in upcoming sessions, effects would mirror those of SB 3—billions in lost revenue, mass retail closures (especially for THC-reliant vaping shops), and shifts to black markets or out-of-state sales. Stricter regulations (e.g., potency caps or licensing) could mitigate some harm by allowing limited sales but might still reduce profits by 20–50% for retailers through compliance costs. Conversely, if regulation prevails, the industry could stabilize, fostering job growth (as seen in recent wage increases) while addressing safety issues. The ongoing legal gray area ensures volatility, with the Texas Supreme Court’s pending rulings on related cases potentially influencing outcomes.

Strategies for Shopping Center Owners with Vaping Shop Tenants

Shopping center owners and commercial landlords in Texas face significant risks from potential THC bans or regulations, as vaping and smoke shops—many of which derive over 50% of profits from hemp-derived THC products—could shutter, leading to widespread vacancies. Similar to leasing to cannabis-related tenants, landlords must proactively manage these risks through lease structuring, diversification, and contingency planning. Below are key strategies, drawing from commercial real estate best practices for high-risk retail sectors like cannabis.

- Review and Strengthen Lease Agreements: Incorporate protective clauses in new or renewed leases, such as requirements for tenants to comply with all federal, state, and local laws (including future changes), and “escape clauses” allowing early termination if legislative shifts (e.g., a THC ban) render the business unviable. Consider shorter lease terms (e.g., 3-5 years instead of 10+) with options for renewal based on performance, and include provisions for higher security deposits or personal guarantees from tenants to cover potential defaults. For existing leases, audit for boilerplate compliance requirements that could trigger eviction or renegotiation if laws change.

- Ensure Compliance with Property Restrictions and Financing: Before renewing leases, investigate zoning laws, deed restrictions, or loan covenants that might prohibit cannabis-related activities (including hemp THC sales, which operate in a legal gray area). Confirm that leasing to such tenants won’t violate mortgage terms or trigger lender recalls. If risks are high, negotiate with lenders for waivers or refinance to more flexible terms.

- Enhance Insurance and Risk Management: Require tenants to carry elevated insurance levels (e.g., higher liability and property coverage) to protect against claims related to product liability or regulatory violations. Landlords should also review their own policies for exclusions like “criminal acts” that could deny claims if tenants’ operations are deemed illegal under federal law. Consider specialized cannabis or high-risk retail insurance riders to cover potential vacancies or damage from tenant closures.

- Diversify Tenant Mix and Reposition Properties: Reduce dependency on vaping shops by actively recruiting stable, non-cannabis-related tenants such as experiential retail (e.g., fitness studios, entertainment venues, or food concepts) that drive foot traffic and are resilient to online competition. For spaces vacated by at-risk tenants, consider merging units into mixed-use configurations, like combining retail with residential or co-working spaces, to attract broader appeal. In a soft commercial market, leverage this to negotiate favorable terms with new tenants.

- Develop Vacancy Contingency Plans: Build financial reserves (e.g., 6-12 months of operating expenses) to cover short-term voids, and create marketing strategies for reletting spaces quickly—such as pre-listing properties or partnering with brokers specializing in retail repositioning. Monitor tenant financial health through regular reporting requirements in leases, and prepare for evictions by avoiding common pitfalls like improper notices.

- Monitor Legislation and Engage in Advocacy: Track Texas legislative sessions via resources like the Texas Legislature Online or industry groups (e.g., Texas Real Estate Commission or commercial real estate associations) to anticipate changes. Join coalitions advocating for regulations over bans, as these could allow tenants to adapt rather than close. Consult legal experts in cannabis and real estate law for scenario planning, including potential challenges to bans under federal preemption.

The following table outlines prioritized actions with timelines:

By implementing these measures, shopping center owners can mitigate the economic fallout from potential tenant failures, turning vulnerabilities into opportunities for property repositioning in a evolving retail landscape.

Strategies for Vaping Shops to Prepare for Potential Future Impacts

Texas retail owners in the hemp, vaping, and smoke shop sectors face ongoing uncertainty due to repeated legislative attempts to ban or heavily regulate THC products. Based on industry analyses and retailer experiences, proactive steps can mitigate risks. Key recommendations include:

- Diversify Product Offerings: Shift inventory toward non-intoxicating alternatives like CBD-dominant products (e.g., flower, edibles, oils, and tinctures with minimal THCA), CBG, CBN, CBC, or emerging cannabinoids such as THCP, which may not be targeted by current bans and can provide similar effects. Explore Delta-8 or HHC where compliant, and expand into non-hemp items like smoking accessories or wellness products to reduce dependency on THC revenue, which often exceeds 50% for vaping shops.

- Ensure Regulatory Compliance and Documentation: Maintain detailed lab certificates of analysis (COAs) for all products to verify they meet the 0.3% Delta-9 THC limit, conduct regular audits, and train staff on compliance. Register as a retail hemp seller with the Texas Department of State Health Services (DSHS) if not already done, and prepare for potential inspections by building relationships with local inspectors and suppliers who provide tested products.

- Monitor Legislation and Engage in Advocacy: Stay informed by tracking bills on the Texas Legislature website, joining industry groups like the Texas Hemp Coalition or U.S. Hemp Roundtable, and participating in forums. Lobby lawmakers through associations to push for regulation over bans, and consider contributing to political efforts supporting hemp-friendly policies.

- Build Financial and Operational Resilience: Stockpile compliant inventory with shorter lead times for flexibility, optimize cash reserves to weather closures, and explore scalable ordering or private-label options for quick pivots. Develop customer loyalty programs emphasizing education on hemp benefits to retain sales during transitions.

- Prepare Contingency Plans: Consult attorneys for legal guidance on potential lawsuits against the state, as many retailers plan to challenge bans under federal Farm Bill protections. Consider relocating operations to hemp-friendly states like Oklahoma or New Mexico, shipping excess inventory out-of-state, or pivoting to online sales (while navigating interstate laws). If a ban passes, liquidate THC stock before effective dates (e.g., January 1, 2027, for similar prior bills) to avoid criminal penalties.

- Explore Medical Cannabis Opportunities: With Texas’s expanded medical program in 2025, investigate partnerships or transitions to licensed dispensaries for low-THC medical products, which could provide a regulated alternative revenue stream.

These strategies emphasize adaptability, as outright bans could lead to closures, while regulations might allow continued operations with adjustments.

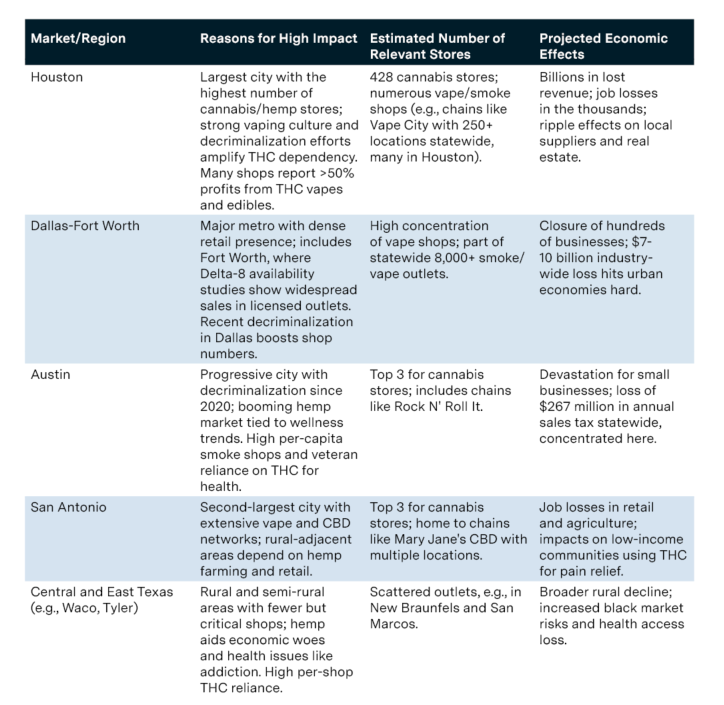

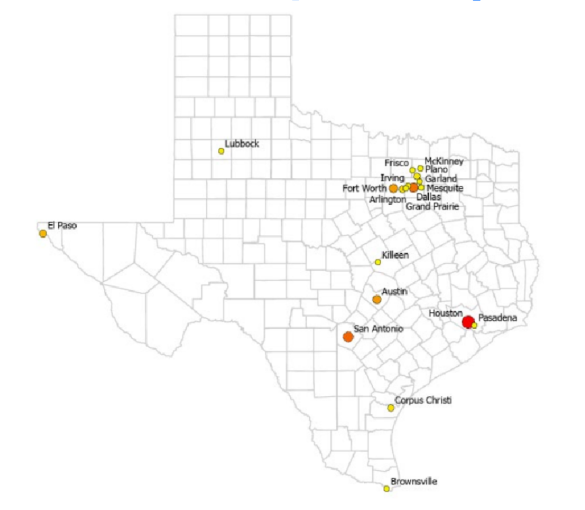

Texas Markets Most Likely to Be Negatively Impacted

The potential ban on THC products would disproportionately affect regions with high concentrations of vape shops, smoke shops, and hemp retailers, where THC sales drive significant economic activity. Urban areas dominate due to population density and consumer demand, but some rural regions also rely on hemp for economic and health benefits. Based on data from business directories, industry reports, and studies, the most impacted markets include:

Part II: Texas Senate Bill 840 – Zoning Reform Impact

Texas Senate Bill 840 and Its Impact on Commercial Real Estate Investment and Development

Texas Senate Bill 840 (SB 840), signed into law by Governor Greg Abbott on June 20, 2025, and effective September 1, 2025, represents a transformative shift in zoning regulations for multifamily and mixed-use residential development in Texas’s largest cities. This supplemental report, building on prior discussions about Texas and Atlanta commercial real estate (CRE) markets, the One Big Beautiful Bill Act (OBBBA), and Texas’s housing shortage, focuses on SB 840’s provisions and their implications for CRE investment and development, with an emphasis on multifamily housing and office-to-residential conversions. It also estimates the economic impact from 2025 to 2027, particularly in major Texas markets like Dallas-Fort Worth, Houston, Austin, and San Antonio.

SB 840 is a game-changer for Texas CRE, unlocking multifamily and mixed-use development in commercial zones and easing office-to-residential conversions. By 2027, it could drive $10-15 billion in investment, add 100,000-150,000 housing units, and create significant economic activity in Dallas-Fort Worth, Houston, Austin, and San Antonio. However, developers must navigate oversupply risks, local resistance, and financing hurdles to capitalize on this opportunity. Combined with OBBBA’s tax incentives, SB 840 positions Texas as a leader in addressing housing shortages through innovative CRE development.

Key Provisions of SB 840 Impacting Commercial Real Estate

SB 840 applies to municipalities with populations over 150,000 in counties with populations exceeding 300,000, covering approximately 19 Texas cities, including Dallas, Fort Worth, Houston, Austin, San Antonio, McKinney, Frisco, Irving, Plano, and Arlington. The bill streamlines multifamily and mixed-use development by removing zoning barriers and reducing regulatory costs. Below are the key provisions and their CRE impacts, informed by prior conversations about Texas’s housing shortage (over 300,000 units) and market trends in Dallas-Fort Worth and Houston.

- By-Right Multifamily and Mixed-Use Development

- Details: SB 840 mandates that municipalities allow multifamily (three or more dwelling units) and mixed-use (at least 65% residential) development in zones designated for office, commercial, retail, warehouse, or mixed-use without requiring rezoning, variances, or public hearings. Permits must be approved administratively if they meet municipal land development regulations.

- Impact on CRE:

-

- Multifamily: This provision eliminates time-consuming and costly rezoning processes, enabling developers to build multifamily projects in commercial corridors where housing demand is high but land availability is limited. In Dallas-Fort Worth, where multifamily vacancy rates reached 11.2% in Q1 2025 due to oversupply, SB 840 could accelerate projects in high-demand submarkets like Uptown and Preston Center, leveraging their strategic locations. In Houston, with a 26.5% office vacancy rate, developers can target underutilized commercial sites for multifamily development, addressing the state’s housing shortage of over 300,000 units.

-

- Mixed-Use: The bill encourages mixed-use projects, enhancing walkability and asset value in urban and suburban areas. For example, a vacant retail site in West Frisco could increase from 82 units (19 units/acre) to 156 units (36 units/acre) without public hearings, boosting project feasibility.

- Eased Office-to-Residential Conversions

- For buildings at least five years old being converted to multifamily or mixed-use (at least 65% residential), SB 840 prohibits municipalities from requiring traffic impact analyses, mitigation fees, more than one parking space per unit, utility upgrades beyond minimum capacity, design standards beyond the International Building Code, or impact fees (e.g., building permits, parkland dedication).

- Impact on CRE:

-

- Office Conversions: The provision targets underperforming office buildings, particularly Class B and older Class A properties struggling with post-pandemic vacancy rates (e.g., 26.1% citywide in Houston, Q4 2024). In Dallas-Fort Worth, submarkets like the West End, , could see office-to-residential conversions accelerate, especially for buildings with high vacancy (25.2% DFW average).

-

- Cost Savings: Waiving fees and studies reduces soft conversion costs by 10-15%, making projects financially viable in markets with high construction costs (e.g., 1-2% increase due to tariffs). In Houston’s Pearland/South submarket, where office demand is growing, conversions could stabilize multifamily submarkets by repurposing obsolete office stock.

- Density and Height Flexibility

- Details: Municipalities cannot cap multifamily density below the greater of 36 units per acre or the highest residential density allowed in the city (e.g., 175 units/acre in Plano). Height restrictions must allow the greater of 45 feet or the maximum height for commercial buildings on the site. Setbacks are limited to the lesser of zoning code requirements or 25 feet, and floor area ratios (FARs) are unrestricted

- Impact on CRE:

-

- Multifamily: Higher density allowances enable larger projects in land-constrained urban areas, such as Dallas’s Pepper Square or Austin’s infill locations. In San Antonio (17.7% office vacancy, $24.29/SF rent), developers can maximize unit counts on commercial sites, addressing housing demand driven by population growth (Texas projected at 32.5 million by 2030).

-

- Mixed-Use and Retail: The flexibility supports mixed-use hubs in suburban areas like Frisco or McKinney, where retail contraction (e.g., vacant strip malls) creates opportunities for residential integration. This aligns with national trends toward adaptive reuse, as noted in prior discussions about retail dynamics in Texas.

- Exemptions and Limitations

- Details: SB 840 exempts areas near heavy industrial zones, airports, military bases, or accident potential zones to mitigate conflicts. Municipalities retain authority to regulate short-term rentals, enforce water quality standards, and offer voluntary incentives like density bonuses. The bill also allows fees for building safety inspections in conversions.

- Impact on CRE: These exemptions limit development in high-risk areas, ensuring compatibility with surrounding uses. However, they may constrain opportunities near industrial zones in Houston or Dallas-Fort Worth, where industrial demand (e.g., shallow bay, outdoor storage) is strong due to acquisitions by firms like Brookfield and Alterra. Voluntary incentives could encourage affordable housing in markets like Austin, complementing OBBBA’s LIHTC provisions.

Economic Impact Estimates (2025-2027)

SB 840 is expected to significantly boost CRE investment and development in Texas, particularly in multifamily and office-to-residential conversions, by reducing regulatory barriers and costs. Below are estimates for 2025-2027, drawing on prior discussions about Texas’s housing shortage, Dallas-Fort Worth’s multifamily trends, and Houston’s office market dynamics.

- Multifamily Sector

- Impact: SB 840’s by-right approvals and density flexibility could unlock 45-150 projects annually across 11 DFW cities (e.g., Dallas, Fort Worth, Plano), adding 4,500-43,500 units by 2027. Statewide, the bill may facilitate 100,000-150,000 new units, addressing 33-50% of Texas’s 300,000-unit shortage. In high-demand markets like Austin and Dallas, projects in commercial zones could increase multifamily investment by 12-15% ($6-8 billion annually).

- Challenges: Oversupply risks in Dallas-Fort Worth (11.2% vacancy in Q1 2025) and tariff-driven cost increases (1-2%) may pressure rents, requiring developers to target high-demand submarkets like Uptown or Frisco. Local resistance, as noted in Dallas’s Pepper Square, could prompt new municipal regulations by late 2025, narrowing the development window.

- Office-to-Residential Conversions

- Impact: The bill’s fee waivers and streamlined approvals could spur 20-50 office conversion projects annually in Houston, Dallas-Fort Worth, and Austin, adding 2,000-5,000 units by 2027. In Houston, where Class B offices face 26.1% vacancy, conversions could absorb 5-10% of vacant stock, stabilizing the market. Investment in conversions may reach $1-2 billion annually, driven by cost savings and housing demand.

- Challenges: High interest rates (8.6% for CRE loans in 2025) and tenant lease complications (e.g., renewal options) may delay projects. Financing hurdles, as noted in prior discussions about Brookfield’s acquisitions, could limit conversions of smaller properties with high churn.

- Mixed-Use and Retail Redevelopment

- Impact: SB 840’s provisions could drive $2-3 billion in mixed-use investment annually, particularly in suburban markets like Frisco and McKinney, where vacant retail sites (e.g., Sprouts pads) are prime for conversion. In San Antonio, mixed-use projects could enhance walkability, supporting retail segments like fitness and experiential dining, as seen in prior Texas retail trends.

- Challenges: Infrastructure strain (e.g., schools, traffic) and community opposition, as voiced in Dallas, may lead to new local rules, impacting project feasibility. Compatibility concerns in planned development districts like Pepper Square could limit density gains.

- Overall Economic Contribution

- Estimate: SB 840 could generate $10-15 billion in CRE investment across Texas by 2027, with 60-70% in multifamily and mixed-use projects. Job creation may reach 20,000-30,000 annually, driven by construction and related industries. Property tax revenues could increase by $100-200 million due to higher-density developments, though the Legislative Budget Board notes fiscal neutrality for the state.

- Regional Focus: Dallas-Fort Worth and Houston will lead due to their scale and housing demand, with Austin and San Antonio benefiting from infill opportunities. The bill complements OBBBA’s LIHTC and QOZ provisions, amplifying affordable housing and Opportunity Zone investments in areas like Firefly Park.

Strategic Implications and Risks

SB 840 offers significant opportunities for CRE investors and developers, particularly in multifamily and office conversions, but strategic planning is critical:

- Act Quickly: Developers should initiate projects before September 2025 to leverage the bill’s streamlined approvals, as cities like Dallas may impose new regulations by late 2025.

- Target High-Demand Submarkets: Focus on areas like Uptown, Preston Center, or Austin’s infill zones to mitigate oversupply risks and maximize returns.

- Leverage Cost Savings: Use fee waivers and reduced studies to lower project soft costs, especially for office conversions in Houston and Dallas-Fort Worth.

- Monitor Local Responses: Anticipate municipal pushback, as seen in Dallas’s planning department testimony, and engage with legal counsel to navigate evolving regulations.

Risks:

- Market Saturation: Oversupply in Dallas-Fort Worth’s multifamily sector could depress rents, as noted in prior discussions.

- Infrastructure Strain: Increased density without traffic or school mitigation may lead to congestion and public opposition, as highlighted by critics like Marc Lombardi.

- Financing Challenges: Lenders may hesitate to fund conversions without clear budgets for demolition or utilities, especially for smaller properties.

SB 840 is a game-changer for Texas CRE, unlocking multifamily and mixed-use development in commercial zones and easing office-to-residential conversions. By 2027, it could drive $10-15 billion in investment, add 100,000-150,000 housing units, and create significant economic activity in Dallas-Fort Worth, Houston, Austin, and San Antonio. However, developers must navigate oversupply risks, local resistance, and financing hurdles to capitalize on this opportunity. Combined with OBBBA’s tax incentives, SB 840 positions Texas as a leader in addressing housing shortages through innovative CRE development.

Steve Triolet

Senior Vice President of Research and Market Forecasting

[email protected]

tel 214 223 4008