Executive Summary

Q4 in Review

Although healthy population growth and a growing consumer base continued to underpin industrial demand in Metro Atlanta, leasing activity declined by 8.7% quarter-over-quarter (QOQ) in Q4 2025 to 9.4 million sq. ft. However, the decline was not widespread and largely confined to Airport/South Atlanta, where leasing slowed 41.1% QOQ to 1.4 million sq. ft. partially offsetting the slowdown was strong leasing activity in I-85 North, which led all submarkets with 3.5 million sq. ft. of transactions—a modest 0.4% drop from the previous quarter. Momentum was further supported by I-20 West, where leasing increased by 6.8% from the prior quarter to 1.5 million sq. ft., and I-75 North, which recorded a 22.8% uptick to 869,617 sq. ft.

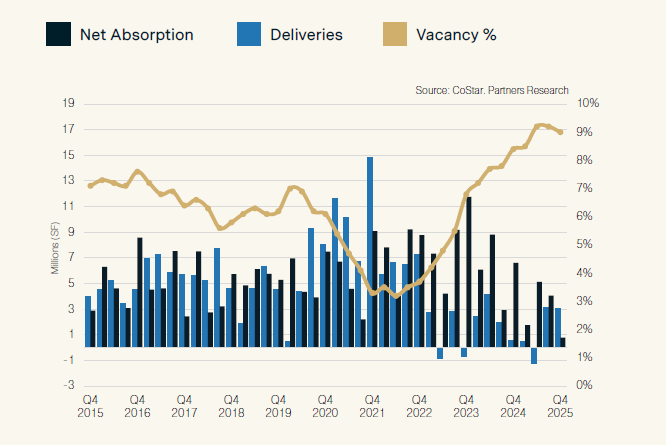

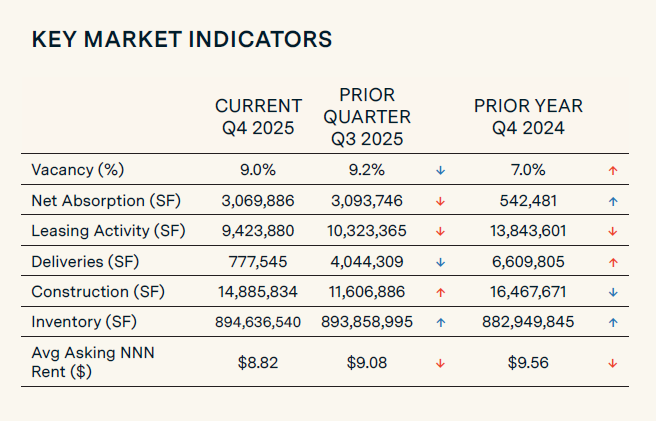

Net absorption totaled 3.1 million sq. ft. in the fourth quarter, mirroring the prior quarter’s performance and signaling ongoing recovery from the negative absorption recorded during the first half of the year. Anchored by increased occupancy, the overall vacancy rate declined by 20 basis points (bps) QOQ in Q4 2025 to 9.0%. The improvement was further supported by a sharp pullback in new construction, with developers delivering just 777,545 sq. ft. in Q4— the lowest quarterly total in more than 11 years. Limited deliveries of high-quality space tempered rent growth, with asking rates easing 2.9% from the preceding quarter to $8.82 per sq. ft., a three-year low. While a historically constrained construction pipeline is expected to limit near-term annual rent growth in 2026, the lack of new supply positions the metro for further vacancy compression in the quarters ahead.

SUPPLY & DEMAND

KEY MARKET INDICATORS

MARKET OVERVIEW

ATLANTA ECONOMIC UPDATE

Metro Atlanta’s labor market continued to expand in November, though employment growth eased to 0.3% year-over-year (YOY). Hiring was limited by the trade, transportation and utilities sector, which contracted by 1.9% from a year earlier. However, the labor market sustained strong payroll growth in other industries, such as education and health services (+4.7%) and leisure and hospitality (+2.9%). The manufacturing sector boasted annual employment growth of 1.2% in November, reflecting underlying resilience despite ongoing tariff-related pressures tied to foreign supply-chain dependencies. The momentum is poised to persist as electrical equipment manufacturer Socomec is adding 300 jobs as part of its Gwinnett County expansion. Moreover, animal health company Zoetis will invest $600 million into a new Douglasville manufacturing facility slated to house 100 new jobs, while pharmaceutical manufacturer ACG plans to create 200 jobs as part of a $200 million expansion of its Newton County plant. These investments underscore continued momentum in Metro Atlanta’s economy and highlight the outsized role of the region’s industrial base.

LEASING ACTIVITY RECORDED MIXED RESULTS

Leasing activity totaled 40.2 million sq. ft. in 2025, down 19.6% YOY as occupiers grew more selective amid macroeconomic uncertainty and limited availability in preferred locations. The pullback was most pronounced in Airport/South Atlanta and I-75 North, where leasing volumes fell 39.1% to 6.7 million sq. ft. and 35.7% to 4.5 million sq. ft., respectively. By contrast, demand remained resilient in I-85 North, which recorded 12.9 million sq. ft. of leasing in 2025—down just 1.4% from the prior year—underscoring its position as the market’s primary demand driver. The submarket boasted 30 leases over 100,000 sq. ft. for the year, led by the 1.1-million-sq.-ft. Williams-Sonoma renewal at the Braselton Commerce Center in August and the 839,712-sq.-ft. Coleto Brands extension at Jefferson Distribution Center in June. Leasing also strengthened in select secondary submarkets, with activity rising by 42.1% in Stone Mountain and 8.2% in I-85 South.

OCCUPANCY LEVELS REBOUNDED

After a sharp slowdown in net absorption during the first six months of the year, momentum rebounded in the second half, with 3.1 million sq. ft. of occupancy gains in both the third and fourth quarters. Net absorption was heavily concentrated in I-85 North, which tallied 4.4 million sq. ft. of occupancy growth, helping offset nearly 4.0 million sq. ft. of occupancy loss in Airport/South Atlanta. I-85 South emerged as a late-year driver of occupier demand, posting 2.1 million sq. ft. of net absorption in 2025, with more than 1.6 million sq. ft. occurring in the fourth quarter alone. The uptick spurred a 450-bps drop in vacancy within I-85 South. Metro-wide, the overall vacancy rate declined by 20 bps QOQ to 9.0%, the second consecutive quarter of either flat or declining vacancy.

CONSTRUCTION PIPELINE SLOWED

The construction pipeline remained at historically low levels with 14.9 million sq. ft. of product taking shape at the close of Q4 2025. I-75 North emerged as the most active submarket with more than 4.6 million sq. ft. under construction, largely pre-leased to major manufacturing users in projects such as the 3.3 million-sq.-ft. Hyundai SK Battery Plant in Kingston and the 500,000-sq.- ft. Qcells production facility in White. Both developments are expected to deliver in Q1 2026. SK Innovation is also building a 430,000-sq.-ft. manufacturing facility in I-85 North, where 3.1 million sq. ft. was under construction in the fourth quarter, 20.8% of which is pre-leased. Meanwhile, I-75 South had 2.8 million sq. ft. underway at quarter close, with pre-leasing limited to 18.8%, underscoring the high volume of speculative development in the submarket.

INVESTOR ACTIVITY REMAINED STRONG

Total sales volume in Metro Atlanta’s industrial sector exceeded $1.5 billion in Q4 2025, marking the second-largest quarterly total in the past four years, trailing only Q3 2025, when more than $1.5 billion in assets traded hands. Investor demand pushed the average sale price up sharply by 34.5% QOQ to a new all-time high of $146.49 per sq. ft., while average cap rates expanded by 40 bps to 7.3%. The quarter’s largest transaction was the $253.0 million sale of a 15.2-MW, fully occupied data center at 4905 North Point Parkway, acquired by GI Partners from Principal Real Estate Investors. The asset traded at nearly four times its prior sale price in 2022, underscoring sustained investor demand for digital infrastructure. Additional momentum was evident in the logistics sector, highlighted by the $133.0 million sale of The Cubes at Bridgeport – Building D, a newly delivered 1.2-million-sq.- ft. distribution facility in Newnan, which traded from CRG to QTS Realty Trust, Inc. at $110.72 per sq. ft. Industrial sale activity is expected to remain strong over the next year, supported by strong tenant demand and a waning construction pipeline.

For More Information, Contact:

Alex Kaplan

SVP of Research

tel 404 850 0667

[email protected]