Metro Atlanta Office Market Sustains Momentum: Strong Q4 Leasing and Record Rents Signal 2026 Stability

EXECUTIVE SUMMARY

Stable fundamentals persisted in the Metro Atlanta office market in the fourth quarter as total leasing exceeded 2.2 million sq. ft. Central Perimeter outpaced all submarkets with 464,571 sq. ft. of total leases signed, up 23.1% from the preceding quarter. Central Perimeter’s Q4 performance was powered by Infor’s 82,000 sq. ft. sublease at Campus 244 and GoToFoods Group extending for 74,049 sq. ft. at MidCity Plaza. Midtown posted 365,168 sq. ft. of leasing, up 18.0% quarter-over-quarter (QOQ). Midtown leasing was driven by Kilpatrick Townsend’s 148,112-sq.-ft. renewal at 1100 Peachtree and two sizable leases at Regions Plaza: Regions Bank (22,892 sq. ft.) and New South Construction (22,456 sq. ft.).

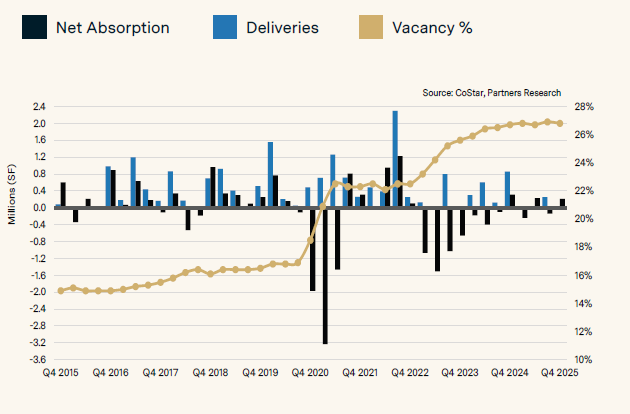

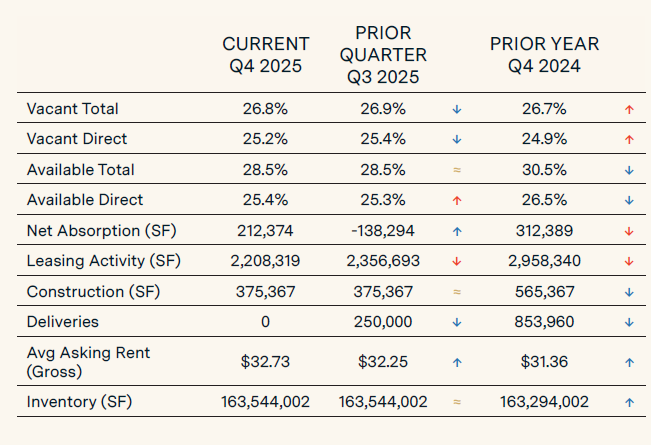

Atlanta documented 212,374 sq. ft. of net absorption in the fourth quarter, bolstered by occupancy growth of 194,946 sq. ft. in Buckhead and 178,324 sq. ft. in North Fulton. In tandem, the overall vacancy rate declined by 10 basis points (bps) QOQ to 26.8% with five submarkets boasting a drop in vacancy for the quarter. Consistent occupier demand, coupled with the absence of speculative office construction, has kept vacancy in check. No new office product delivered in Metro Atlanta during the fourth quarter, while just 332,000 sq. ft remained under construction. Despite the slowdown in new development, overall asking rents continued their steady upward accent, increasing by 1.5% from the prior quarter to $32.73 per sq. ft. (psf), a new historic high. While rent growth remained most pronounced in Class A product, Class B buildings recorded a 1.0% increase in rents for the quarter, reflecting broad-based market health. Together, sustained leasing activity, positive absorption, and a constrained development pipeline signal ongoing stability across Atlanta’s office market in 2026.

SUPPLY & DEMAND

KEY MARKET INDICATORS

MARKET OVERVIEW

ATLANTA ECONOMIC UPDATE

Job growth in the Atlanta Metro edged up by a modest 0.3% year-over-year (YOY) in November, a deceleration from year-ago levels amid ongoing job loss in the information sector. However, the labor market sustained positive momentum in other industries as robust payroll growth persisted in education and health services (4.7%) and leisure and hospitality (2.9%).

Atlanta also continued to demonstrate resilience amid a new wave of corporate relocations and expansions. AMX Logistics will establish its U.S. headquarters in West Midtown, a move that is expected to create 200 jobs. Salesforce plans to expand its local headcount with the addition of 250 jobs at its offices along East Paces Ferry Road. In Sandy Springs, Mercedes-Benz will create 500 new jobs at its U.S. headquarters, joining a growing roster of companies expanding or relocating to Central Perimeter. Driven by a deep talent base and sustained population growth, Atlanta remains wellpositioned for continued economic expansion amid macroeconomic uncertainty.

LEASING ACTIVITY REMAINED STABLE

Propelled by a strong fourth quarter, total leasing activity in Metro Atlanta during 2025 totaled 8.7 million sq. ft. With over 1.6 million sq. ft. of annual leasing, Central Perimeter emerged as the metro’s top-performing submarket and the only one to surpass 300,000 sq. ft. of leasing each quarter. TriNet taking 145,186 sq. ft. of space at the Perimeter Center and High Street aided the submarket’s impressive year. North Fulton boasted 1.6 million sq. ft. of total transactions in 2025, mirroring the prior year’s total. While the lion’s share of tenant demand in North Fulton remained concentrated in Alpharetta, neighboring Johns Creek captured one of the largest leases of the year: Boehringer Ingelheim’s 73,900-sq.-ft. renewal at the Medley mixed-use development. In Buckhead, 20 leases over 20,000 sq. ft. were signed in 2025, propelling the annual leasing total to 1.3 million sq. ft. The annual performance was powered by Greenberg Traurig, renewing for 110,374 sq. ft. at Terminus 200, and CoStar extending their 82,131-sq.-ft. space at Phipps Tower.

OCCUPANCY LEVELS STRENGTHEN

Atlanta documented 62,676 sq. ft. of net absorption in 2025, a change of pace from the 371,221-sq.-ft. of negative absorption in 2024. Seven of Atlanta’s 11 submarkets recorded occupancy gains for the year, led by 244,880 sq. ft. of net absorption in the Northwest. The submarket has tallied 542,273 sq. ft. of net absorption during the past two years combined, more than any other submarket during that period. The expanding amenity base surrounding Truist Park, home of the Atlanta Braves, has bolstered occupancy of top-tier product in the Northwest, a trend unfolding across the metro. Premium buildings recorded 723,343 sq. ft. of net absorption in 2025 and more than 100,000 sq. ft of occupancy growth in eight of the past nine quarters. Premium assets in Buckhead generated occupancy growth of 308,843 sq. ft. in 2025, the largest total in Metro Atlanta.

VACANCY RATE DECLINED

The overall vacancy rate in the Central Business District declined by 60 bps QOQ to 30.6%. Buckhead drove the improvement, as elevated occupancy reduced the submarket’s vacancy by 110 bps to 28.8%. Buckhead’s performance more than offset a modest 10-bps increase in Midtown, where a thinning construction pipeline is expected to exert downward pressure on vacancy in the coming year. Meanwhile, overall vacancy in suburban Atlanta increased slightly by 20 bps compared to the prior quarter to 24.3%. The increase was triggered by the Northeast and Central Perimeter submarkets, where rates rose by 100 bps to 21.1% and 80 bps to 29.1%, respectively. However, the Northwest submarket registered a 70-bps drop to 20.0% amid sustained occupier demand in Cumberland/Galleria. In the increasingly inventory-constrained North Fulton submarket, the overall vacancy rate declined by 50 bps QOQ to 27.4%, the third consecutive quarterly drop.

RENTAL RATES CONTINUED TO INCREASE

Overall rental rates in the Atlanta Metro totaled $32.73 psf in Q4 2025, up 1.5% QOQ and 4.4% from Q4 2024. Rent growth was strongest in Buckhead, where asking rates climbed 7.5% year-over-year (YOY) to $40.46 psf. This milestone marks the first time rents have exceeded $40.00 psf in the submarket, underscoring continued pricing momentum among top-tier assets. Rents continued to rise in the Northwest, increasing by 3.6% QOQ to $29.56 psf. Growing supply constraints in the Northwest have increased landlords’ pricing power, especially for updated, well-located assets. As return-to-office mandates proliferate throughout the metro, landlords are expected to continue pushing asking rents higher, while relying on concessions to secure tenant commitments.

INVESTMENT SALES VOLUME IMPROVED

Year-to-date sales volume across Atlanta totaled nearly $1.2 billion in 2025, representing a 12.3% increase over 2024. The average sale price held firm YOY at $211 psf, while the average cap rate compressed to 7.8%—down from 8.6% in 2024 but above the five-year average of 7.6%. Alkamy Capital’s $38 million acquisition of the 499,968-sq.-ft. Crown Pointe office complex in Central Perimeter marked the largest transaction of the fourth quarter. The sale reflects a significant repricing, with Pacific Oak Strategic Opportunity REIT exiting the asset at approximately 54.0% below its 2017 acquisition cost of $83 million.

For More Information, Contact:

Alex Kaplan

SVP of Research

tel 404 850 0667

[email protected]